Introduction

पहिली पगाराची SMS नोटिफिकेशन दिसते आणि हृदय जोरात धडधडायला लागतं…

आणि पहिला प्रश्न —

“पहिली नोकरी मिळाल्यावर करायच्या आर्थिक गोष्टी कोणत्या?”

काय आधी करायचं? बचत? गुंतवणूक? EMI? Family expenses?

मुंबईतील आदित्यला पहिली Salary ₹22,000 मिळाली.

तो उत्साहातच नवीन मोबाईल घेतो, weekend parties, online शॉपिंग…

महिन्याच्या शेवटी Wallet शून्य!

वर्षभरात काहीही बचत नाही… Stress मात्र वाढलेला! 😞

पहिली नोकरी मिळाल्यावर करायच्या आर्थिक गोष्टी

योग्य पद्धतीने केल्या तर

👉 आर्थिक स्वातंत्र्य मिळेल

👉 कर्जाचा धोका टाळता येईल

👉 Future Goals सहज साध्य होतील

हा मार्गदर्शक तुम्हाला पहिल्या पगारापासून

Financially Strong Life कडे नेईल! 💪💰

Read More

2️⃣ UPI आणि Digital Payments सुरक्षित कसे वापरायचे?

3️⃣ Credit Score वाढवण्याचे 10 सोपे मार्ग

4️⃣ EMI म्हणजे काय? फायदे-तोटे – मराठी मार्गदर्शक

5️⃣ Budget कसे बनवावे? Step-by-step मराठी

पहिली नोकरी म्हणजे काय? (Financial Meaning)

पहिला पगार म्हणजे —

फक्त पैशाची सुरुवात नाही,

तर आर्थिक जबाबदारीची सुरुवात!

| घटक | सत्य |

| Money earned | आता तुमच्या हातात |

| खर्च | तुमच्या निर्णयावर |

| Future | तुमच्या planning वर depend |

➡ आयुष्यभराचा आर्थिक स्वभाव — या क्षणात ठरतो!

पहिली नोकरी मिळाल्यावर आर्थिक प्लॅनिंग का महत्त्वाचं?

| कारण | परिणाम |

| Early planning | जास्त संपत्ती |

| Compounding | कमी पैशांत मोठा फंड |

| Savings discipline | कर्जमुक्त जीवन |

| Investing early | Retirement stress-free |

| Unexpected expenses | Emergency fund saves |

➡ आता केलेलं planning = भविष्यातील Peace of Mind

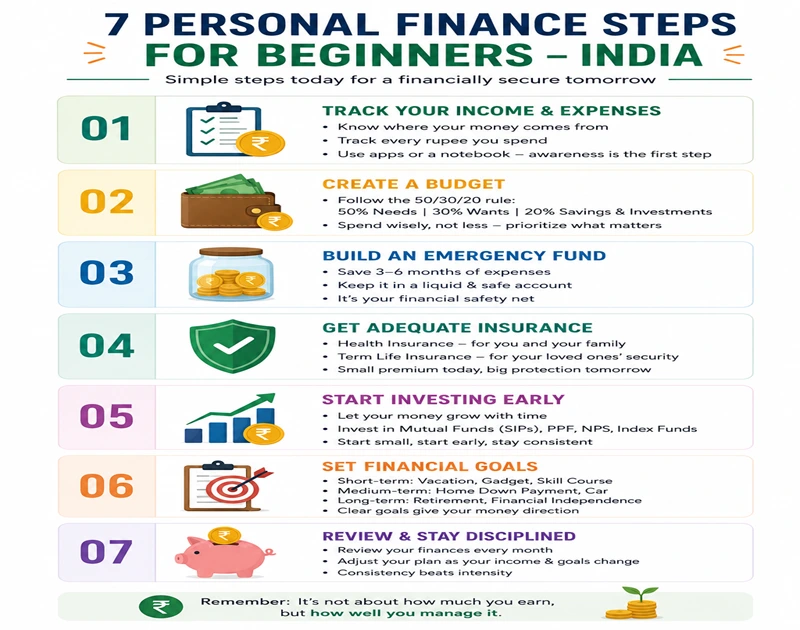

पहिली नोकरी मिळाल्यावर करायच्या आर्थिक गोष्टी — Overview Table

| Step | आर्थिक गोष्ट | तुमच्यासाठी फायदा |

| 1 | Budgeting & Expense tracking | Control & clarity |

| 2 | Emergency fund तयार | सुरक्षा आणि शांत झोप |

| 3 | Health Insurance त्वरित | मोठ्या खर्चापासून बचाव |

| 4 | SIP Investment सुरू | Wealth building |

| 5 | Credit Score Build | Future loans easy |

| 6 | कर्ज टाळा / Control | Stress-free life |

| 7 | Skills & Courses मध्ये गुंतवणूक | Income वाढ |

➡ ह्या “7 प्रवासाची” सुरुवात = पहिल्या पगारापासूनच! 🔥

Read More

2️⃣ UPI आणि Digital Payments सुरक्षित कसे वापरायचे?

3️⃣ Credit Score वाढवण्याचे 10 सोपे मार्ग

4️⃣ EMI म्हणजे काय? फायदे-तोटे – मराठी मार्गदर्शक

5️⃣ Budget कसे बनवावे? Step-by-step मराठी

भारतातील Young Earners — Reality Check (Data + Authority)

| आकडेवारी | स्रोत | Message |

| 70% Indian youth → No Savings | Times of India | Money mismanaged |

| 55% spend full salary monthly | ET Survey | No future planning |

| Only 6% invest in SIPs | AMFI | Knowledge gap |

| Medical expenses → 68% debt cases | RBI | Insurance ignored |

➡ डेटा सांगतो:

पैसा कमावणे सोपे… सांभाळणे अवघड!

पहिली नोकरी मिळाल्यावर कोणता खर्च महत्त्वाचा?

| खर्च | Priority |

| Food + Travel | High |

| Parents Support | High |

| EMI for Luxuries | Low |

| Fashion + Parties | Low |

| Skill Development Courses | High |

| Impulsive Online shopping | Avoid |

➡ Priority wrong = Financial Mess

➡ Priority right = Financial Success

Maharashtra Real Story (Case Study)

📍 Priyanka — Pune

Job: IT Support

Salary: ₹28,000/month

तिचे पॅटर्न्स:

- iPhone EMI ✓

- Weekends movie + food ✓

- Savings ✘

3 वर्षांनंतर:

कुठलाही फंड नाही…

CIBIL वर 689 → Personal loan reject ❌

ती म्हणते:

“पैसे कमवले मी… पण पैसा मला सांभाळत होता!”

➡ पहिली नोकरी = First Discipline Test 🎯

Pass = Rich Future

Fail = Struggle Future

Why most new earners fail financially?

Read More

2️⃣ UPI आणि Digital Payments सुरक्षित कसे वापरायचे?

3️⃣ Credit Score वाढवण्याचे 10 सोपे मार्ग

4️⃣ EMI म्हणजे काय? फायदे-तोटे – मराठी मार्गदर्शक

5️⃣ Budget कसे बनवावे? Step-by-step मराठी

| कारण | परिणाम |

| “आता मजा करूया” attitude | No savings |

| Social media show-off | EMI burden |

| Financial knowledge नाही | Wrong decisions |

| Delay in investments | Compounding loss |

| Family dependency समजत नाही | Stress |

➡ Enjoy करा ✨ पण Planning सोबत! 📈

Mindset Shift Formula

(Very Important)

Earn → Save → Spend

❌ उलट नको:

Spend → Save → Earn (not possible)

➡ Rule: Salary येताच 20% Save करा → बचत आधी, खर्च नंतर!

📌 Quick Budget Mantra (Starter Formula)

50 : 30 : 20 Rule

| Percentage | Use |

| 50% | Needs (Rent, Travel, Bills) |

| 30% | Wants (Lifestyle) |

| 20% | Savings + SIP Investment |

➡ Month 1 पासूनच FOLLOW! 💪

Step 1️⃣ — Budgeting & Expense Tracking

(पहिले नियंत्रण… मग प्रगती!)

का?

- Money leaks ओळखण्याचा एकमेव मार्ग

- खर्च कुठे जातो हे कळलं तर बचत वाढते

Practical Action

📌 वापरा: Walnut / CRED / Notion template

📍 Category-wise limit 🎯

- Food: ₹6,000

- Travel: ₹3,000

- Subscription: ₹500

Table — Monthly Budget Sample

Read More

2️⃣ UPI आणि Digital Payments सुरक्षित कसे वापरायचे?

3️⃣ Credit Score वाढवण्याचे 10 सोपे मार्ग

4️⃣ EMI म्हणजे काय? फायदे-तोटे – मराठी मार्गदर्शक

5️⃣ Budget कसे बनवावे? Step-by-step मराठी

| Category | Max Spend |

| Needs | 50% |

| Wants | 30% |

| Savings & SIP | 20% |

➡ नोकरीची सुरुवात Budget शिवाय = गाडी ब्रेकशिवाय 😅

Step 2️⃣ — Emergency Fund तयार करा

(3–6 months rule)

का?

- Job loss? Medical emergency? Travel delay?

- EMI/loan ची वेळेत भरपाई

Example Calculation

Salary: ₹25,000

Emergency Fund Target = ₹75,000–₹1,50,000

| Duration | Monthly Saving | Result |

| 12 months | ₹6,500 | ₹78,000 |

| 18 months | ₹4,500 | ₹81,000 |

➡ Emergency fund = आर्थिक घालमेलवर ब्रेक!

Step 3️⃣ — Health Insurance लगेच घ्या

(Parents वर Depend नको!)

का?

RBI & IRDAI Report:

➡ Medical cost accidents = 68% कर्जाचे कारण ❗

| Situation | Without Insurance |

| Accident Bill | ₹1,50,000 |

| Payout | तुमच्या savings मधून 😰 |

📌 Corporate Medico claim असला तरी separate plan आवश्यक

→ Job बदलल्यावर gap येतो!

➡ Insurance हे Savings protect करणारे कवच! 🛡️

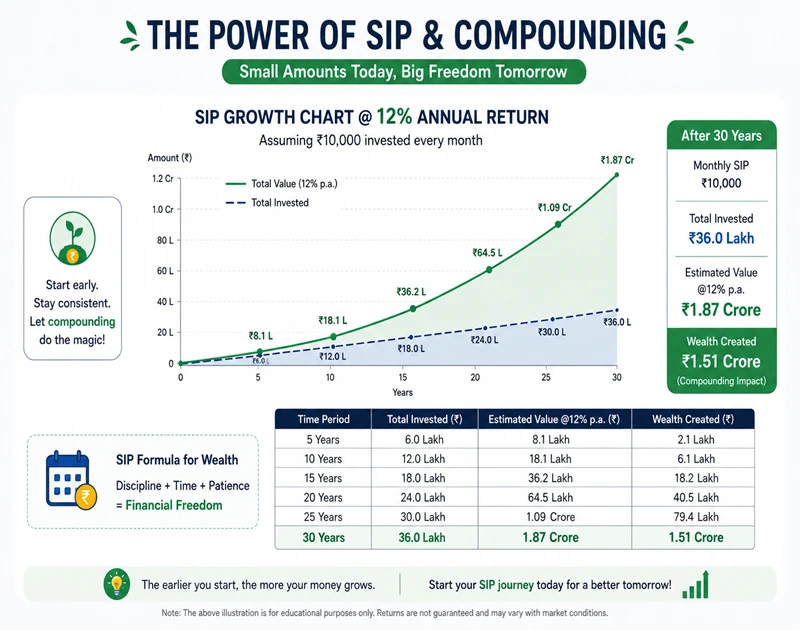

Step 4️⃣ — SIP Investment सुरू करा

(12% Long-term return power)

Read More

2️⃣ UPI आणि Digital Payments सुरक्षित कसे वापरायचे?

3️⃣ Credit Score वाढवण्याचे 10 सोपे मार्ग

4️⃣ EMI म्हणजे काय? फायदे-तोटे – मराठी मार्गदर्शक

5️⃣ Budget कसे बनवावे? Step-by-step मराठी

| SIP | Tenure | Result* |

| ₹1,000 | 10 yrs | ₹2.3 Lakh |

| ₹1,000 | 25 yrs | ₹13+ Lakh |

| ₹2,000 | 25 yrs | ₹26+ Lakh |

(Sensex historical return base)

➡ Compounding = तुमची future ATM मशीन!

🟢 Best Beginner Strategy

Index Fund + Largecap + Hybrid SIP

🏦 Step 5️⃣ — Credit Score Build करा

(Future loans easily मिळण्यासाठी!)

Credit Score कसा वाढतो?

✔ Credit Card बिल time वर

✔ Limit चा 30% usage

✔ No cash withdrawal

| Score | Result |

| >750 | 😎 Easy approvals + Low interest |

| <650 | 😓 Loan reject |

➡ Credit Score = Future Financial Identity

🚫 Step 6️⃣ — कर्ज टाळा / EMI control

(Show-off culture → Debt trap)

| Purchase | EMI Risk | Best Option |

| New iPhone first salary | 🔴 High | Save first |

| Bike EMI | 🟠 Medium | Consider public transport |

| Necessary electronics | 🟢 Low | No-cost EMI OK |

➡ EMI should build assets, not stress!

Step 7️⃣ — Self Investment: Skills & Courses

(Highest ROI investment!)

| Skill | ROI Period |

| English & Communication | 6–12 months |

| Digital skills (Excel/SEO/Design) | 3–6 months |

| Domain certificates | Career booster |

➡ Skill वाढली → Salary वाढली 💰🔥

First Salary Financial Plan — One Page Blueprint

| Action | % | Tool |

| Needs | 50% | Budget app |

| Wants | 20–30% | Cash/UPI |

| Savings + SIP | 20–30% | Auto SIP |

| Insurance | ₹300–₹600 | Health plan |

➡ हा Plan FOLLOW = Future Perfect 🎯

❤️ Maharashtra Real Examples — Motivation Boost

Read More

2️⃣ UPI आणि Digital Payments सुरक्षित कसे वापरायचे?

3️⃣ Credit Score वाढवण्याचे 10 सोपे मार्ग

4️⃣ EMI म्हणजे काय? फायदे-तोटे – मराठी मार्गदर्शक

5️⃣ Budget कसे बनवावे? Step-by-step मराठी

| नाव | शहर | Decision | Result |

| प्रिया | Pune | SIP started ₹1,500 | ₹85k in 4 yrs |

| अमेय | Thane | No insurance → hospital bill | ₹70k loan |

| प्रतीक | Nashik | EMI avoided + skill course | Package double |

➡ Same salary, different decisions → Different LIFE!

❌ Common Mistakes Indians Make (Avoid these!)

| चूक | परिणाम |

| Insurance ignore | Big unexpected loss |

| Only saving, no investing | Inflation loss |

| Salary fully खर्च | No growth |

| Social media lifestyle copying | Debt |

| SIP बंद Market मध्ये | Loss locked |

➡ चुका टाळणे = पैशाची पहिली कमाई 💡

Importance & Benefits Summary

| Benefit | Why critical? |

| Future security | Emergency ready |

| Wealth creation | Compounding जरूरत |

| Peace of mind | Financial stress-free |

| Skill growth | Income boost |

| Creditworthiness | Home/Car loan success |

➡ तुमचं Future तुमच्या आजच्या निर्णयांवर!

📌 Step-by-Step Automation (Zero Failure Financial System)

Money Plan सोपं आहे:

Salary येताच = Auto-Save → Auto-SIP → Auto-Bills

📍 Auto-Flow Formula

| Salary Day | Action | Tool |

| Day 1 | 20–30% Auto Transfer → Savings A/c | Standing Instruction |

| Day 2 | Auto Debit → SIP | Groww / Zerodha |

| Day 5 | Bills Auto Pay | CRED / Bank |

| Day 25 | Expense review | Walnut |

➡ System perfect = तुम्ही हरलात तरी पैसा जिंकतो! 💪✨

What to do with your first salary?

| Priority | खर्च | % |

| #1 | Emergency Fund | 10–15% |

| #2 | SIP Investment | 10–15% |

| #3 | Skills/Certification | 10% |

| #4 | Parents Support | 5–10% |

| #5 | Lifestyle Wants | 20–30% |

| #6 | Needs | 40–50% |

➡ “Save First, Spend Later” हीच Success ची वाट!

Example Calculation #1

Salary ₹25,000 असल्यास → Smart Plan

| विभाग | रक्कम | फायदा |

| Emergency Fund | ₹3,000 | सुरक्षा |

| SIP Investment | ₹3,000 | भविष्यातील संपत्ती |

| Skill Development | ₹2,500 | उत्पन्न वाढ |

| Needs | ₹12,000 | Control |

| Wants | ₹4,500 | Lifestyle |

➡ आजची छोटी रक्कम → उद्याचा मोठा Value!

Example Calculation #2

Future Wealth Calculation (25 yrs SIP)

| SIP ₹ | 12% ROI | Final Value |

| ₹1,500 | Compounding ↑ | ₹49,00,000+ |

| ₹2,000 | More power | ₹65,00,000+ |

| ₹3,000 | Future freedom | ₹1 Crore+ 🏆🔥 |

➡ घर, कार, ट्रॅव्हल — सगळं शक्य! 🌍

Financial Timeline (Milestones)

| वय | Goal |

| 22 | Budget + Insurance + SIP |

| 24 | Emergency Fund Full |

| 26 | Credit Score > 750 |

| 28 | Skill-based salary hike |

| 30 | घरखरेदी Planning start |

➡ Early start → Early Freedom 💼✨

Trusted Apps Recommendation

| Need | Best apps |

| SIP investment | Groww / Zerodha Coin |

| Expense tracking | Walnut / Moneyview |

| Credit Score | CRED / OneScore |

| Insurance comparison | PolicyBazaar |

| Skill Courses | Coursera / Udemy |

➡ Tools Right = Future Bright 💡

Maharashtra Real Case Study

(Emotional Trust Boost)

साक्षी (Nagpur) — First Job: ₹28,000

✔ Auto SIP: ₹3,000

✔ Emergency Fund: ₹1,500

✔ Skill Course: ₹2,000

🎯 3 Years Result:

- ₹1,50,000+ Wealth

- Salary Hike 2X

- Credit Score: 765

ती म्हणते:

“मी पगाराची मालक झाले — पगार माझा मालक नव्हता!” 😎🔥

➡ Decision today → Pride tomorrow!

Smart Rules (Very Important)

Read More

2️⃣ UPI आणि Digital Payments सुरक्षित कसे वापरायचे?

3️⃣ Credit Score वाढवण्याचे 10 सोपे मार्ग

4️⃣ EMI म्हणजे काय? फायदे-तोटे – मराठी मार्गदर्शक

5️⃣ Budget कसे बनवावे? Step-by-step मराठी

| Rule | का महत्त्वाचं? |

| खर्च = पगार – बचत | Retirement सुरक्षित |

| EMI = फक्त Assets ला | कर्जटाळ |

| Credit Card full bill | CIBIL strong |

| Emergency fund 6 months | Peace of mind |

| SIP stop नाही | Wealth continues |

➡ Money works only when YOU control it ✊

🚫 First Salary Mistake Prevention Checklist

| चूक | Result |

| First EMI iPhone | Stress for 12 months |

| Parties + shopping > Savings | No future security |

| Health Insurance ignore | मोठा धक्का |

| Gambling/crypto FOMO | Total loss |

| Zero planning | Constant worry |

➡ मजाही करा… आर्थिक शहाणपणासोबत! 😄

🏁 Final Summary Table

पहिली नोकरी मिळाल्यावर करायच्या आर्थिक गोष्टी — 7 Golden Rules

| क्रमांक | आर्थिक गोष्ट | मुख्य फायदा |

| 1️⃣ | Budgeting | Control & Clarity |

| 2️⃣ | Emergency Fund | सुरक्षा व तणावरहित जीवन |

| 3️⃣ | Health Insurance | मोठ्या खर्चापासून बचाव |

| 4️⃣ | SIP Investment | Future wealth |

| 5️⃣ | Credit Score Build | Loan approvals & lower interest |

| 6️⃣ | EMI & कर्ज टाळा | Stress-free life |

| 7️⃣ | Skills मध्ये गुंतवणूक | Income वाढ, Career growth |

➡ पगाराची सुरुवात = आर्थिक यशाची सुरुवात!

FAQ

1️⃣ पहिली नोकरी मिळाल्यावर करायच्या आर्थिक गोष्टी कोणत्या?

Budget, Insurance, SIP, Emergency fund, Credit score.

2️⃣ पहिली Salary मिळताच SIP सुरू करावी का?

हो! ₹500–₹2,000 पासून सुरुवात उत्तम परिणाम देते.

3️⃣ Emergency Fund किती असावा?

आपल्या Salary च्या 3–6 महिन्यांच्या खर्चाएवढा.

4️⃣ पहिल्या नोकरीनंतर Insurance का घ्यावे?

Medical आणि accident खर्चापासून बचाव.

5️⃣ पहिली नोकरी मिळाल्यावर EMI घेणे योग्य आहे का?

फक्त अत्यंत आवश्यक गोष्टींसाठी, Show-off साठी नाही.

Final Conclusion + Strong CTA

🎯 पहिली नोकरी मिळाल्यावर करायच्या आर्थिक गोष्टी

आता तुम्हाला अगदी स्पष्ट झाल्या आहेत!

आजच सुरू करा:

✔ Budget 💡

✔ Insurance 🛡️

✔ SIP 💸

✔ Emergency Fund 🔐

✔ Skill Growth 🎓

👉 जितक्या लवकर निर्णय…

👉 तितकं मोठं Future!

पगार हा फक्त पैशाचा प्रवाह नसतो…

तो तुमच्या जीवनाच्या प्रगतीचा मार्ग असतो! 💪🔥

➡ आज पाऊल टाका → उद्याचा विजय तुमचाच! 🏆✨